Social Security and Medicare aren’t a package deal. You pick when to start Social Security — anywhere from 62 to 70. Medicare has its own timeline at age 65.

Sign up for these programs at the wrong times, and you could face coverage gaps or higher premiums. Getting the timing right keeps your healthcare costs steady and protects your retirement income.

This guide shows you how to best line up your Social Security and Medicare enrollment. You’ll see the smart moves that boost your benefits, learn what higher earners should watch for with premiums, and spot the timing traps that catch many retirees by surprise.

Medicare enrollment and Social Security benefits: Getting started

Social Security puts money in your pocket each month after you retire. The amount depends on your work history and when you start your benefits. Start at 62 and you’ll get a smaller monthly check. Wait until 70 and you’ll get the maximum amount.

Medicare covers your healthcare costs in retirement. Part A handles hospital stays and inpatient care. Part B covers regular doctor visits, preventive services, and medical equipment. For most people, they are eligible for both parts at 65

Here’s what’s key: Medicare premiums come out of your Social Security check if you’re enrolled in both. And those premiums can change based on your income through something called IRMAA (Income Related Monthly Adjustment Amount).

The good news? Most people get Medicare Part A with zero premiums since they paid Medicare taxes while working. Part B does have a premium — $185 per month in 2025 for most people. But if you’re already getting Social Security when you start Medicare, those premiums get automatically deducted from your monthly check.

IRMAA and Social Security: What higher earners should know

Making over $106,000 as a single filer or $212,000 if married? Your Medicare costs more through IRMAA — an extra charge on top of your regular Part B premium.

Medicare looks at your tax returns from two years ago to set these rates. Your 2025 IRMAA depends on what you earned in 2023. While most people pay $185.00 for Part B, high earners could pay up to $628 per month.

See updated IRMAA for 2025 here

If you get Social Security benefits, both your Part B premium and IRMAA come right out of your monthly check. No Social Security yet? Medicare sends you a quarterly bill instead.

Keep an eye on your income as retirement nears. One-time money moves like selling investments or taking retirement withdrawals could push you into a higher IRMAA bracket. Many people work with financial advisors to time these decisions around Medicare costs.

Social Security and Medicare enrollment: Planning your timeline

Medicare enrollment opens three months before your 65th birthday month. You get until three months after to sign up without penalties. If you’re born in July, your window runs April through October.

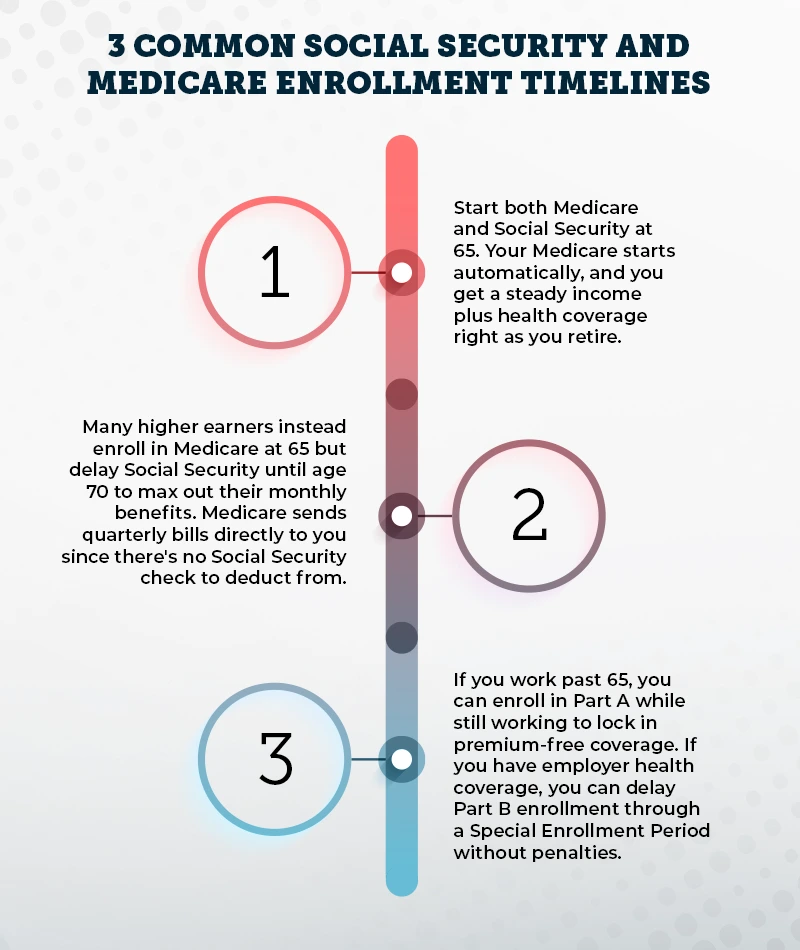

Let’s look at three common timing routes:

- The typical path? Start both Medicare and Social Security at 65. Your Medicare starts automatically, and you get steady income plus health coverage right as you retire.

- Many higher earners take a different route. They enroll in Medicare at 65 but delay Social Security until age 70 to max-out their monthly benefits. During those years, Medicare sends quarterly bills directly to you since there’s no Social Security check to deduct from.

- Working past 65 opens a third option. You can enroll in Part A while still working to lock in premium-free coverage, since delaying Part A might mean paying premiums later. If you have employer health coverage, you can delay Part B enrollment through a Special Enrollment Period without penalties. This lets you keep your workplace coverage until you retire. Just remember that once you stop working or lose that coverage, you have that eight month Special Enrollment Period to sign up for Part B.

Not on Social Security yet? You’ll need to sign up for Medicare yourself. Mark your calendar — missing your enrollment window means paying a penalty added to your monthly premium for every 12-month period you could have had coverage. This penalty is 10% of the base premium Understanding the Medicare enrollment and Social Security impact helps you avoid these costly mistakes.

Avoiding Social Security and Medicare enrollment mistakes

Waiting too long to sign up for Medicare can cost you. If you miss your Initial Enrollment Period without having other qualifying coverage, you will have to pay a penalty for each year you wait.

Income changes can also sneak up on you. A big retirement account withdrawal might push you into a higher IRMAA bracket. Since Medicare uses your tax returns from two years ago, planning ahead helps avoid premium surprises.

Sometimes couples get caught off guard when one spouse retires early. If you’re under 65 and start Social Security, but your spouse is 65 or older, they might miss important Medicare deadlines, thinking coverage is automatic.

Always check with Social Security about your specific situation. They handle Medicare enrollment and can confirm your deadlines and options based on your exact circumstances. Or speak with United Medicare Advisors and we can help you plan for retirement and avoid unnecessary penalties.

Planning ahead: Your Social Security and Medicare enrollment success

Social Security and Medicare enrollment decisions shape your retirement income and healthcare coverage. Starting Medicare at 65 protects you from lifetime penalties, while your Social Security timing affects your monthly benefits amount.

Higher earners face extra considerations with IRMAA affecting their Medicare costs. Understanding how your income impacts premiums two years down the road helps you plan retirement account withdrawals and other income strategically.

Your enrollment path depends on your specific situation — working status, health coverage needs, and retirement goals. Start planning these decisions early and talk with Social Security about your options. Thoughtful retirement planning for Medicare and Social Security ensures you maximize benefits while minimizing costs. Getting the timing right keeps your benefits and coverage steady through retirement.

Disclaimer:

The information provided in this blog post is intended for general informational purposes only and does not constitute medical advice. It is not a substitute for professional medical consultation or treatment. Always consult with a qualified healthcare provider for any questions you may have regarding a medical condition.

United Medicare Advisors does not endorse or recommend any specific products, treatments, or procedures mentioned in this article. Reliance on any information provided in this blog post is solely at your own risk. We encourage you to discuss any health concerns or questions with your doctor before making any decisions about your health, wellness, or treatment.